UBIT and UDFI

Potential Taxes For Your Self-Directed Investments

Typically, you don’t pay taxes on your retirement account earnings or pay capital gains tax on those investments.

However, every responsible investor who self-directs their portfolio should be aware of Unrelated Business Taxable Income (UBTI, with the tax being called UBIT) and Unrelated Debt Financed Income (UDFI), including which investments trigger this type of tax and the solutions for reducing or avoiding it in the future.

What is UBIT and UDFI?

How Does UDFI Work?

Here's An Example

Let’s say you have a $100,000 real estate investment opportunity, which you split 50/50 with $50,000 from your IRA Club self-directed IRA and a non-recourse loan of $50,000.

Now, let’s say that investment, after a period of time, generates $10,000 of income. Because 50% of that investment was used with a non-recourse loan, $5,000 of that net income is now subject to UDFI tax (UBIT).

How to Calculate UBIT

Calculating UBIT can be complex, especially with an income-generations business in your IRA. Below is a simplified calculation and can be much more complicated based on a variety of variables, so we recommend consulting with a knowledgeable CPA that understands both IRAs and unrelated business taxable income to ensure your IRA is paying the correct amount of UBIT.

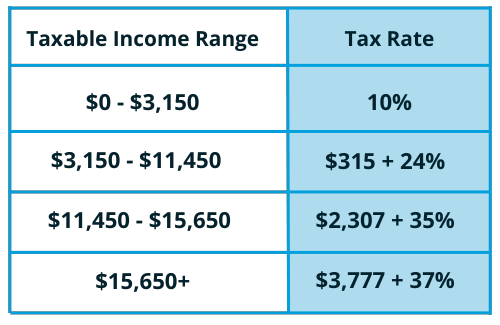

Trust Tax Brackets for 2025 </span<

Calculating UBIT

First, establish your gross income. Once the gross income has been determined, deduct any operating expenses for the year and any exemptions if they apply. This will determine your net income.

UBIT = Net Income * Trust Tax Rate

Remember, this is a simplified calculation. Additional variables will need to be considered when calculating UBIT for your SDIRA’s income-generating business. Consult with a CPA or experienced tax professional.

Will My Investment Trigger UBIT?

Some common examples of investments that are more likely to generate UBIT include: income-generating businesses like restaurants, convenience stores, and Airbnbs, cryptocurrency mining operations, and frequent real estate transactions involving the buying and selling of numerous real estate properties in a year.

Click any button below to find out if your investment might trigger UBIT.

Solutions to the UBIT “Problem”

Having to pay a UBIT tax is not necessarily a bad thing. It means the investment is profitable, but if you’re looking to reduce or lower UBIT tax, consider some of these solutions:

- UBIT tax does not apply to investments into C-Corporations because they are taxed at the corporate level.

- Partnering your available IRA funds with other investors to avoid financing with a non-recourse loan.

- If qualified, use a Solo 401(k) for your investments since they typically don’t have to pay UBIT because they are UDFI exempt.

How Do I File For UBIT?

Should the gross income from your operational business or debt-financed property owned by your retirement account exceed $1,000, your retirement account will have to file an IRS Form 990-T to report its UBIT, meaning you will need your retirement account’s EIN to file.

We recommend speaking with an experienced CPA or tax professional to determine the exact UBIT amount & to file IRS Form 990-T.

IRS Form 990-T is due April 15th.

Have Questions?

FAQS

Because the tax is owed by the retirement account, it is the retirement account’s funds that must be used to pay the UBIT or UDFI taxes.

If you do not have the cash balance in your retirement account, you can transfer or roll over funds from other retirement accounts, sell your investments, or make a contribution. The IRS considers paying UBIT or UDFI with personal funds as a contribution.

Dividends, certain rental income, royalties, interest, profits from the sale of property, and certain income from research activities are excluded in the calculation of UBIT.

Limited Partnerships (LP), Limited Liability Companies (LLC), and investments using a third-party loan that generated UDFI are the most likely investments to incur UBIT. Consult your tax professional before making an investment that could potentially incur UBIT or UDFI.